Business credit reports can help you to evaluate a client’s financial position before you do business with them. But you need to be able to read them and understand the data to get the right insights.

In this article, we’ll show you an example UK business credit report from Experian and show you how to interpret it.

Table of Contents

What is a Business Credit Report?

A business credit report is a document that summarises the financial and credit history of a company. It is compiled by a credit reference agency. In the UK, the main providers are Experian, Equifax, and Creditsafe.

It draws on data from Companies House, court records, and financial filings, and typically includes:

- Credit score

- Recommended credit limit

- Details of any County Court Judgments (CCJs)

- Payment performance data

- Summary of the company’s filed accounts and financial position.

So what information is contained in a business credit report, and how can you use one to decide who is worth shaking hands with and who to avoid?

UK Credit Reference Agencies: Experian, Equifax, and Creditsafe

Business credit reports in the UK are produced by several different agencies, and while the information they draw on is broadly similar, the way they present it can differ.

Experian is one of the most widely used agencies for business credit reports in the UK. Their reports include a credit score out of 100, a recommended credit limit, CCJ data, filed accounts, and payment performance history. The walk-through below uses an Experian report.

Equifax provides similar information but uses a different scoring methodology. Their business credit scores run from 0 to 1,000, with higher scores indicating lower risk. They also include director history, which can be useful for identifying connections between companies.

Creditsafe is widely used by credit control teams and is known for its payment performance data, which draws on a large network of trade payment references. If understanding how a business actually pays its suppliers (rather than its theoretical credit score) is your priority, Creditsafe’s payment data can be useful.

For most purposes, any of the three will provide enough information to make a decision.

Credit Report Insights Explained

Here’s a real company credit report that we obtained from Experian. Keep in mind that this is a standard report for a UK business, and reports for other countries will vary.

No Cost. No Obligation.

100% Confidential.

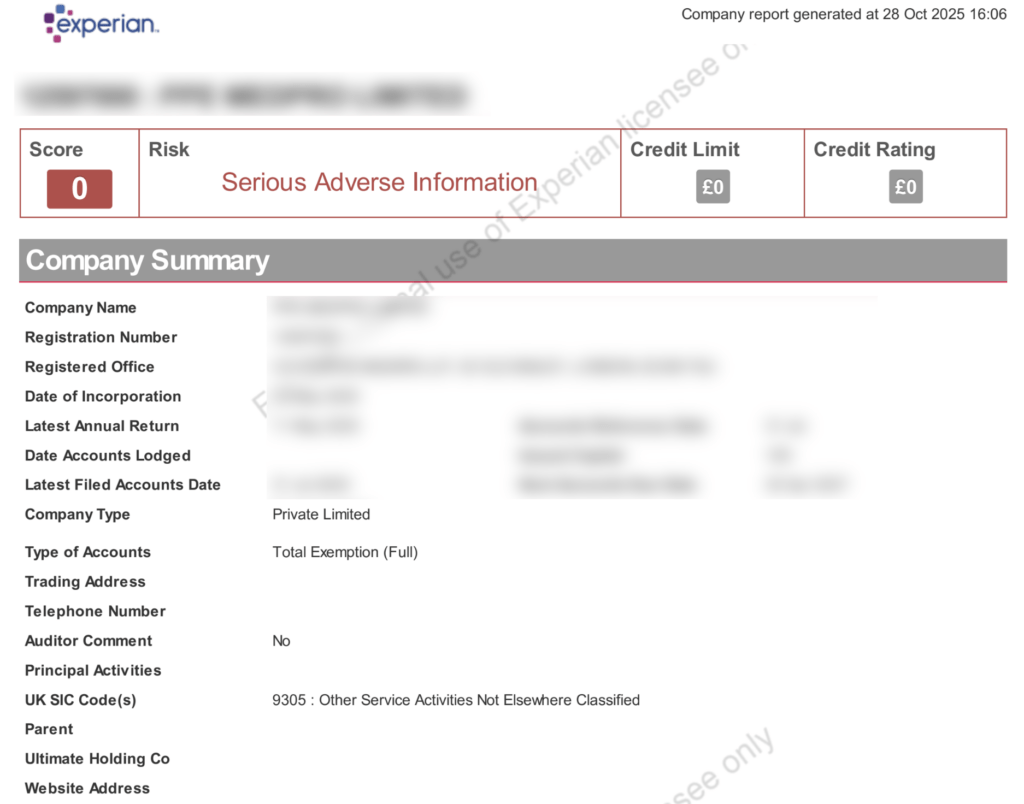

Company Summary

The first section in a standard business credit report is the Company Summary, which provides you with some information about the company’s incorporation, accounts filed, address, and contact details.

Credit Score

At the top of the report, you’ll see a credit score or rating. This provides a key at-a-glance summary of a business’ financial and credit history.

Typically, a credit score will rate a company out of 100 on the likelihood of it paying debts quickly and fairly, with 100 being a ‘perfect’ debtor. The score will usually be displayed graphically, often using a red, amber, green colour coding system.

Additional information provided may include:

- Limiting Factors: Details from the company’s credit history that have lowered the score. These may include serious adverse information such as details of CCJs and writs against the company.

- Risk summary: A short statement summarising the anticipated risk of non-payment in words.

- Risk comparison: Placing the company’s credit score in the context of default risks across that industry.

No credit score may be given in instances where there has been a bankruptcy associated with the business, or where there is insufficient information available.

Credit Limit

The credit report will usually recommend a maximum credit limit for a business, based on overall liabilities and financial performance.

This gives potential creditors an idea of a ‘safe’ level of business a partner should be able to pay for, and what would be overstretching them.

Company Summary

In this section of the credit report, you’ll want to review corporate information such as:

- Registered names

- Addresses

- Contact details

- How long the business has been operating

- Their Indentity History, such as alternative operating names and addresses. This provides a safeguard against businesses with a poor credit history changing their name.

Use this information to verify that your client is who they say they are. Also, check there is no association with other businesses with a poor credit history.

The report will also list details of holding and subsidiary companies, including linkages to any overseas operations, along with details of current and previous directors. This latter information is important to flag up any instances where company directors have filed for bankruptcy.

Accounts

Credit reports sometimes include details of business accounts going back up to five years. This again gives a picture of the financial health of a business, which is useful for weighing up the risks of supplying them.

Change History

Scrolling down the report, you’ll come to the Change History section. This is a timeline of events, including some routine entries (like the filing of accounts), plus more noteworthy changes, like credit scores being reduced.

If you see that the company has been placed into administration, that’s an obvious warning sign that you should avoid doing business with them.

But there are other patterns to look for, such as Credit Risk Score decreasing, Credit Risk Band changing for the worse, or accounts not being filed on time. That could indicate that the company is having financial issues. If you see patterns of decline, you can use that information to decide whether you want to supply them or not.

In some cases, you may find it easier to review score changes in a chart, which is provided further down in the report. We’ll explain that here later.

Mortgages

The mortgages section of a business credit report includes a Summary of Mortgages, Charges and Satisfactions, which is a list of debts the company has.

A charge means that security is being held against company assets. The lender can claim those if the business defaults on the loan. A satisfaction is a debt that has been fully repaid.

In this section, look for outstanding or partially satisfied loans and mortgages. This will give you an idea of the company’s debts.

Risk Summary

The Risk Summary is a concise summary of the credit report in plain English, which may make a recommendation on whether you should deal with them or not.

In some cases, like our example credit report, the summary is clear and direct.

Adverse Credit

This section shows any CCJs that have been issued against the company, and any administration orders.

Score History

The score history is a visual representation of Credit Score Changes and Credit Limit Changes over time. In our example credit report, the change is sudden and pronounced. In other reports, there may be a trend over time.

Payment Performance

The Payment Performance section will tell you whether a company pays its suppliers and creditors on time.

You may see the average days late, percentage paid on time (within 30, 60, or 61+ days), and trends in payment habits.

Financial Summary

The business credit report breaks down financial performance in a number of different sections, which are fairly self explanatory:

- Summary

- Profit And Loss

- Balance Sheets

- Cashflow

- Financial Notes

- Ratios

- Growth

- Industry Comparison

Use these sections to drill down into the financials and examine the company’s finances in different areas.

Company Structure

This final section of the report breaks down the company’s relationship with any other companies it’s associated with. It lists all Company Directors and Shareholders.

How to Make Decisions Based on a Company Credit Report

When reading a company credit report, it’s important to read the whole document and take it as a sum of its parts. If a section is blank, it does not necessarily mean you are safe, since there may be red flags in other areas.

In addition, some of the information on the report will come from Companies House, which means it won’t be verified. The extra information on a credit report can be helpful. For example, reviewing the company’s credit score history is usually worthwhile when taking on any new client.

If you see conflicting information, or you’re already having issues getting paid, contact us for a free review of your situation. Our experienced debt advisors can help you to decide your next step.