When you sign up a new customer or client, it’s tempting to skip the formalities. New customers are always keen, and it seems like nothing can go wrong.

If you ask for a deposit, are you at risk of scaring them away? The answer is no.

Most businesses are used to paying deposits, especially if they are dealing with freelancers or microbusinesses, and there are plenty of good reasons that you should ask for one.

No Cost. No Obligation.

100% Confidential.

Table of Contents

1. Measuring the Commitment of the Client

If your client pays you a deposit, it proves that they are serious about the work, and committed to the working relationship.

If they stall or make excuses, they might be planning to hang on to their cash until they decide that you’re ‘worthy’ of being paid.

Remember: some clients initially seem enthusiastic but can disappear or dodge invoices when it’s time to actually pay you. Initially, a deposit is reassurance that they have the money to pay you and are committed to seeing through the arrangement.

2. Reducing Risk Exposure

At Safe Collections, we frequently chase tiny invoices owed to freelancers and sole traders. Large companies are used to delaying payment, finding excuses not to pay, or subjecting small businesses to long payment cycles.

If a relationship goes bad, and a client goes AWOL, this can result in months of chasing bad debts. And for a small amount of work, it may not even be affordable to chase in the first place.

This is especially true with clients based in another country.

Your client may assume you’ll roll over under pressure and write off an unpaid amount, so it’s a calculated risk for them. If you can decrease your exposure at the start, you’re reducing the risk of letting a rogue client try it on, which means you’re less likely to need us for debt recovery.

3. Easing Cashflow

Large businesses try to hold on to their cash as long as possible. Paying you on the latest possible date is one of the tactics they’ll try. It makes their books look better, and it’s essentially free credit for them.

Depending on your point of view, it may also be a bullying tactic.

Getting a deposit upfront means part of the fee is in your bank for longer, so it’s your cash flow that benefits. Not only do you get the interest, but you also have cash upfront for materials or software that’s necessary to actually start the work.

4. Verifying Business Details

What is the exact name and legal status of your new client? Often, small businesses leave these important details until it’s too late.

It’s critical that you know the exact legal status and identity of your client at the start of any business relationship. If you don’t know who or what you are dealing with it is impossible to identify the risk involved in offering credit.

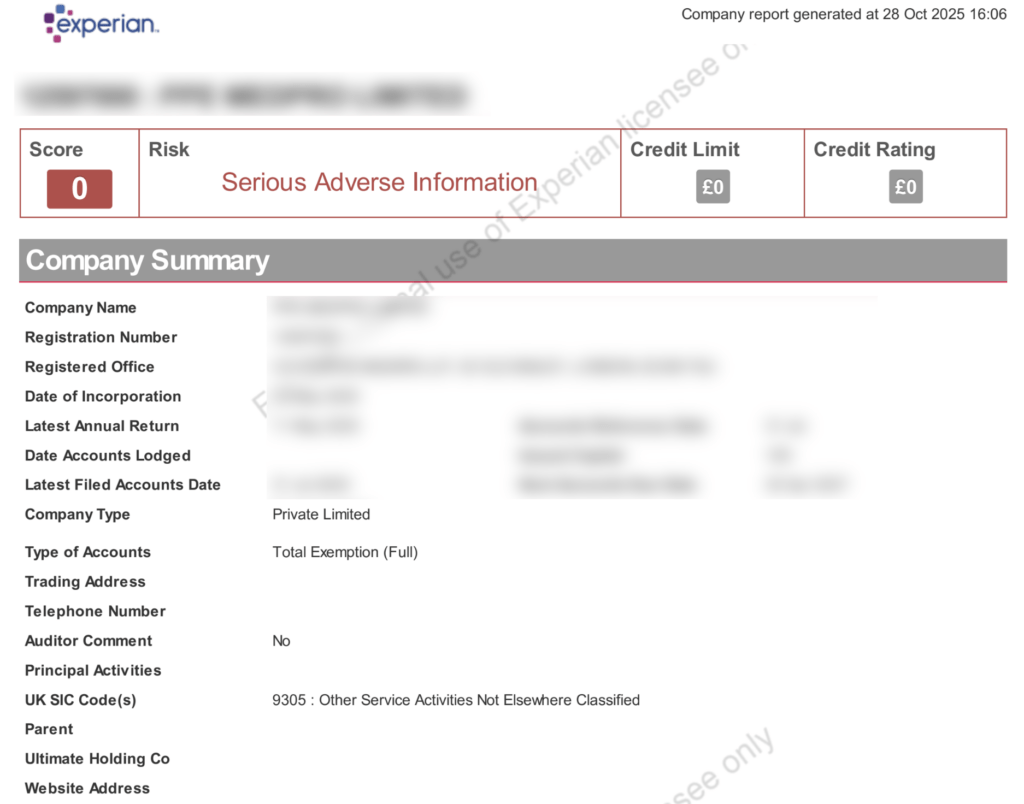

Get all the information from your client, then get a copy of their business credit report and make sure everything matches. Look out for red flags, like low credit scores. We’ve got a guide on how to read a business credit report that will help.

5. Verifying Payment Details

Asking for a deposit allows you to clarify payment information and processes before work starts.

Your client will need to set you up as a payee on whatever systems they use, and they’ll need your bank details. In return, you’ll need the details of the person who actually sends the money.

This is helpful, because it means everything is set up in advance of work being done. This reduces the risk of unpaid invoices in the future.

It also gives you a chance to review the client’s payment processes, including how organised they are and whether they have a dedicated person or department who will deal with your invoices in the future.

If the client has a chaotic approach to payments, or can’t pay your deposit on time, that’s one of the red flags you should watch out for when taking on new work.

What’s a Reasonable Deposit to Ask For?

Requesting 50 percent upfront is reasonable, or even expected, when dealing with larger companies.

If you haven’t worked with the client before and they run a small business, they may have reservations about paying so much. If you sense reluctance, ask for 25 percent at first, and then follow this with staged milestone payments at 50 percent, 75 percent, and 100 percent.

If it’s difficult to work out, just start with a deposit and follow with weekly invoices on very short credit terms. 30 days is standard, but you can agree to 14 days or even same-day payment if your client accepts it.

This allows you to closely monitor your credit risk and manage your cashflow.

And remember: even the most profitable business can quickly slip into financial difficulty, so a perfect payer may become a problem client down the line. If that happens, we’re here to help you on a “no collection – no commission” basis.

Contact us for advice and a free review of your claim.