Do you need to calculate interest on late payments in the UK?

Use our free late payment calculator at the top of this page to work out how much you’re owed.

Overdue invoices are one of the biggest worries facing small business owners. Trying to recover outstanding debts can feel like a very lonely process if you are not aware of the available help.

As a creditor, the law is on your side. Since 1998, UK businesses have been legally entitled to charge interest on late payments owed by another company.

Table of Contents

How UK Law Protects Businesses Against Late Payments

UK businesses are protected by the Late Payment of Commercial Debts (Interest) Act 1998. This law allows you to charge interest on late payments. The UK was the first country in the EU to pass a law that allows you to charge interest on late payments.

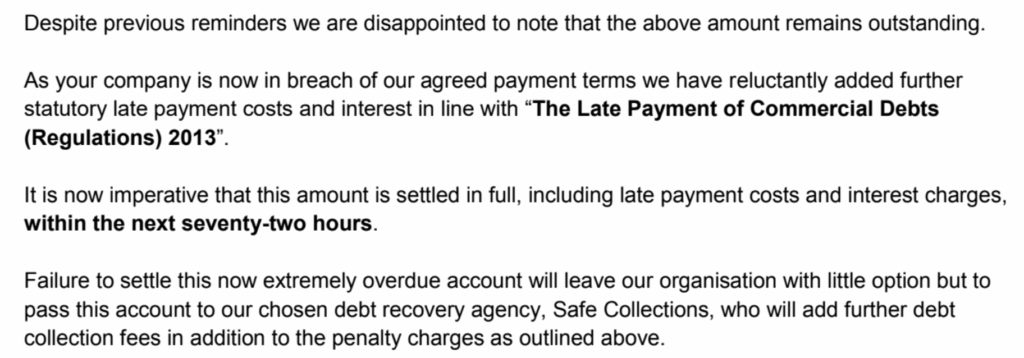

In 2013, the legislation was strengthened to allow businesses to charge debtors for costs incurred for debt recovery.

In practice, this means that hiring a debt recovery agency is essentially free for you under our No Collection = No Commission promise, as long as the debt is recovered along with the additional late payment penalties.

No Cost. No Obligation.

100% Confidential.

When to Add Late Payment Charges and Interest

An invoice is considered overdue the day after the agreed credit period ends.

If you didn’t agree any payment terms, the default is 30 days after your invoice was issued.

That’s why, on our late payment interest calculator (at the top of this page), we’ve set a default of 30 days, but you can change it.

In practice, most businesses come to an agreement between themselves on payment terms, which is acknowledged in the law. Private businesses can agree to terms of up to 60 days, while public authorities must generally pay within 30 days.

If your client wants to extend their due date beyond 60 days, there has to be express agreement from both sides that you consider this fair, and any extended credit must not be “grossly unfair to the creditor.” The legislation itself stops short of actually specifying what constitutes gross unfairness.

How to Calculate Late Payment Interest

Use our free late payment interest calculator at the top of this page to calculate the interest you are owed for an overdue invoice.

To explain how the late interest calculator works, there are two components.

- The interest you are allowed to charge on late payments is calculated by statutory interest, which is 8%.

- Then, we add the current Bank of England base rate for business transactions. For example, the rate is 4% in October 2025. You can check the current base rate on the Bank of England website. (Our calculator has it pre-configured).

Adding those numbers, if the current base rate is 4%, that means you can charge interest at 12% per year.

Converting the Annual Rate to a Daily Rate

Next, you need to convert that annual interest rate into a daily rate because you charge interest each day the invoice is overdue.

To find that daily amount, calculate 12% of the total debt and divide by 365:

Daily Interest = (Total Debt x 0.12)

365

If your invoice has been overdue for a while, calculating the interest can be challenging because the base rate changes.

If this applies to you, we’d be happy to calculate this for you in a free claim review.

No Cost. No Obligation.

100% Confidential.

How to Claim Late Payment Charges

Businesses chasing late payments are legally entitled to claim late payment charges. This means you can charge ‘reasonable costs’ for recovery from the debtor, in addition to the interest they’re owed.

In addition, since 2013, companies have also been able to charge a fixed fee for late payment by way of compensation. In our late payment interest calculator, you’ll see these listed as the fixed penalty fee, and that is added on top of the interest on late payment.

The rates are as follows:

| Outstanding Amount | Fixed Penalty Fee |

| Up to £999.99 | £40 |

| £1000 to £9999.99 | £70 |

| £10,000 and over | £100 |

Informing Clients That You Charge Late Payment Fees

In the UK, adding interest to overdue invoices is your right. As a supplier, you don’t have to notify your clients that you intend to charge late payment interest in advance. If they don’t pay you on time, you can charge it.

That said, you might want to add a reminder to your standard terms and conditions, contracts, or work agreements. That way, your client will know you’re aware of your legal rights.

If you use our free late payment letter templates, you’ll notice that we refer to late fees in the final reminder letter.

You can use this template if you want to give your client some warning that late payment fees may be added, but you don’t have to.

How to Add Interest and Fees to a Late Invoice

You don’t necessarily need to add late payment fees to your existing invoice. You will normally issue a separate invoice when you charge late payment fees, interest, or compensation for a late payment.

This can be complicated because you don’t know how much late payment interest to charge before they pay. So in practice, once you receive agreement to pay, or the original debt is paid off, you would need to issue a new invoice to your client detailing the additional charges payable.

However you choose to do it, remember that penalties are only charged once, at the point when the debt is settled.

Charging International Clients Late Payment Fees

If you are thinking about charging late payment fees for a client outside the UK, contact us for a free review of your situation. We can advise you on the process and whether the recovery of interest and fees is likely to be successful.

Should I Charge VAT on Late Payment Interest?

No. VAT is not applicable on either the interest or fixed cost element of the penalties and must not be charged on your invoice.

You’ll typically mark the line item as “Zero”, “Zero Rated”, or “0%”.

Getting Help With Late Payments or Overdue Invoices

If you still haven’t paid, or your requests for late payment fees are ignored, get in touch with Safe Collections for a free claim review.

Since 1984, Safe Collections has been helping businesses recover what they’re owed. We can often collect on a “No Collection = No Commission” basis.

And whether your clients are in the UK or overseas, we can assist you.